Quarterly Market Report

30th April 2025

1. Macroeconomic developments

Tanzania’s economy continued to demonstrate resilience in April 2025, underpinned by steady growth in the agriculture, construction, and financial services sectors. The GDP growth rate is projected at 5.3% for 2025, supported by public infrastructure investments, a rebound in tourism, and strong performance in mobile money and digital financial services. Inflation remained relatively contained, averaging 3.9%, largely due to stable food supplies and energy prices. The government maintained fiscal discipline, with ongoing efforts to broaden the tax base and streamline public spending. However, the Tanzanian shilling came under slight depreciation pressure against the U.S. dollar due to rising import bills and seasonal demand for foreign currency. Investor sentiment remains cautiously optimistic, especially as regulatory reforms in the capital markets and real estate sectors take shape.

2. Market Overview

In April 2025, the Tanzanian capital market showed a mixed performance compared to March 2025, showing strong activity in the primary bond market, while experiencing a decline in the secondary bond market and equity turnover. The equity turnover dropped sharply while trading volumes increased, driven by a block trade in DCB Commercial Bank (DCB) shares. Although government bond auctions were oversubscribed, reflecting solid investor confidence and appetite, secondary bond trading slowed, indicating a shift towards retail participation. Local investors continued to dominate both buying and selling, with limited foreign involvement and a modest net outflow.

3. Equity Market Performance

3.1 Index Movement

The DSE All Share Index (DSEI) posted a gain, closing at 2,284.14 by the end of April 2025. This represents a decrease of -68 basis

points compared to the end of March 2025 and a year-on-year growth of 27.9% from April 2024.

The Tanzania share index also gained, closing at 4922.18 by the end of April 2025. This represented an increase of 81 basis points compared to the end of March

2025 and a year-on-year growth of 10.7% from April 2024.

3.2 Turnover & Volume

Data suggest a notable divergence between turnover and the volume traded during April 2025. The Dar es Salaam Stock Exchange (DSE) recorded a turnover of TZS 30.9 billion, reflecting a substantial 49% decrease compared to March 2025. In contrast, the volume of shares traded increased by 53% over the same period. This was primarily driven by the block trade on the DCB Commercial Bank counter, which accounted for 44% of the total shares traded but only 5.5% of the total turnover for April 2025.

Figure 1: Equities Counter Contributions

3. Bond Market Update:

Auction results during March 2025 suggest a healthy fixed-income market, with a favourable demand outlook,

well-anchored yield expectations, and increasing in investors’ confidence in longer-duration instruments.

March 2025 witnessed robust activity in the bond market, particularly in the primary segment. The Bank of

Tanzania (BoT) successfully auctioned two new government bonds- a 5-year bond at 13% coupon rate and- a 15-

year bond at 14.5% coupon rate. Both issues were oversubscribed, with total tenders amounting to TZS 198.8

billion for the 5-year bond and TZS 262.4 billion for the 15-year bond. The weighted average coupon yields were

13.0677% and 14.6268% respectively.

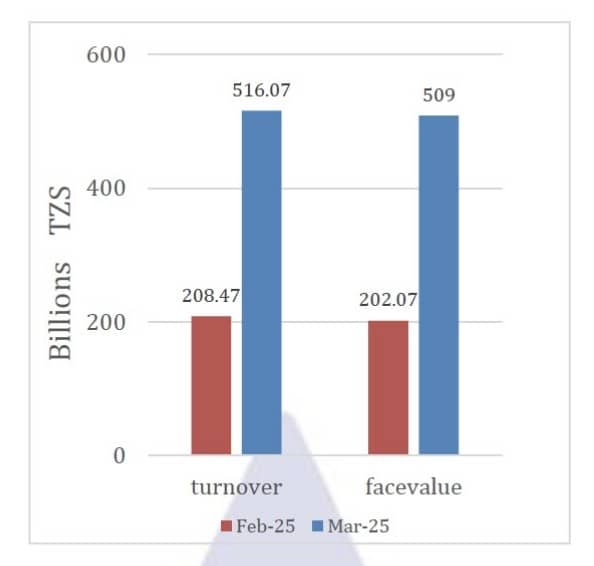

The secondary bond market experienced a substantial uptick in activity during March 2025 compared to the

previous month. The total face value of bonds traded surged to TZS 509 billion, up from TZS 202.07 billion in

February, while turnover rose sharply to TZS 516.07 billion, compared to TZS 208.47 billion. This reflects an

impressive growth of approximately 152% in face value and 147% in turnover. Additionally, the number of

transactions increased from 351 to 406, indicating heightened investor participation and improved market

liquidity.

In short, March 2025 marked a significant expansion in Tanzania’s secondary bond market, characterized by increased investor participation, stronger liquidity, and rising confidence. This trend supports broader capital market development and reflects positively on the effectiveness of monetary and fiscal policy in stabilizing and growing the economy.

4. Investor Participation

Local investor continued to dominate the Market on both the demand and supply side, the participation of the local investor was 98.6% and 60.03% on the demand and supply side respectively while the foreigner participated by 1.3% and 39.97% respectively resulting to a foreign outflow of TZS 23,4 billion

Best Regards,

Research & Financial Analytics,

Tel: +255 762 367 347

Mob: +255 763 631 999

Email: research@alphacapital.co.tz

Twitter:https://x.com/AlphacapitalTz?t=syMgdAEZeWzsqqPcanh5gQ&s=08

LinkedIn:https://www.linkedin.com/company/alpha-capitaltz/

WhatsApp Group:https://chat.whatsapp.com/E7W8BuWZj7eGqXghy

DOWNLOAD THIS REPORT